NEW TRIPOLI, USA: The solar market is huge. After a relatively moderate 2009 where installations grew by only 24 percent, the global PV market roared back to life in 2010, where the 17 GW of installations exceeded the previous years’ 7.1 GW by a stunning 139 percent. With an average annual growth forecast at greater than 40 percent, opportunities to get into the market have never been better.

Part 1 of “Everything you wanted to know about Solar Cells” discusses the different technologies and the market implications for existing and future equipment and materials suppliers to solar cell manufacturers. Part 2 will describe the manufacturing processes of each type of solar cell and the equipment and materials used in production.

How they work?

Nearly all solar cells work the same way – a semiconductor material utilizing a p-n junction to convert sunlight into electricity, as shown in Fig. 1.

Source: The Information Network, USA.

Source: The Information Network, USA.Light travels in packets of energy called photons. The generation of electric current happens inside the depletion zone of the PN junction. The depletion region is the area around the PN junction where the electrons from the N-type silicon, have diffused into the holes of the P-type material.

When a photon of light is absorbed by one of these atoms in the N-Type silicon it will dislodge an electron, creating a free electron and a hole. The free electron and hole has sufficient energy to jump out of the depletion zone. If a wire is connected from the cathode (N-type silicon) to the anode (P-type silicon) electrons will flow through the wire. The electron is attracted to the positive charge of the P-type material and travels through the external load (meter) creating a flow of electric current.

The hole created by the dislodged electron is attracted to the negative charge of N-type material and migrates to the back electrical contact. As the electron enters the P-type silicon from the back electrical contact it combines with the hole restoring the electrical neutrality.

Types of solar cells

Crystalline Solar Cells

By far, the most prevalent bulk material for solar cells is crystalline silicon (abbreviated as a group as c-Si), also known as "solar grade silicon". Bulk silicon is separated into multiple categories according to crystallinity and crystal size in the resulting ingot, ribbon, or wafer.

Monocrystalline silicon (c-Si): often made using the Czochralski process. Single-crystal wafer cells tend to be expensive, and because they are cut from cylindrical ingots, do not completely cover a square solar cell module without a substantial waste of refined silicon. Hence most c-Si panels have uncovered gaps at the four corners of the cells.

Poly- or multicrystalline silicon (poly-Si or mc-Si): made from cast square ingots — large blocks of molten silicon carefully cooled and solidified. Poly-Si cells are less expensive to produce than single crystal silicon cells, but are less efficient. US DOE data shows that there were a higher number of multicrystalline sales than monocrystalline silicon sales.

Ribbon silico is a type of multicrystalline silicon: it is formed by drawing flat thin films from molten silicon and results in a multicrystalline structure. These cells have lower efficiencies than poly-Si, but save on production costs due to a great reduction in silicon waste, as this approach does not require sawing from ingots.

Thin film solar cells

Thin-film technologies reduce the amount of material required in creating a solar cell. Though this reduces material cost, it may also reduce energy conversion efficiency. Thin-film silicon cells have become popular due to cost, flexibility, lighter weight, and ease of integration, compared to wafer silicon cells.

A cadmium telluride solar cell use a cadmium telluride (CdTe) thin film, a semiconductor layer to absorb and convert sunlight into electricity. The cadmium present in the cells would be toxic if released. However, release is impossible during normal operation of the cells and is unlikely during fires in residential roofs. A square meter of CdTe contains approximately the same amount of Cd as a single C cell Nickel-cadmium battery, in a more stable and less soluble form.

Copper indium gallium selenide (CIGS) is a direct-bandgap material. It has the highest efficiency (~20 percent) among thin film materials (see CIGS solar cells). Traditional methods of fabrication involve vacuum processes including co-evaporation and sputtering.

Gallium arsenide multijunction cells were originally developed for special applications such as satellites and space exploration, but at present, their use in terrestrial concentrators might be the lowest cost alternative in terms of $/kWh and $/W. These multijunction cells consist of multiple thin films produced using metalorganic vapor phase epitaxy.

A triple-junction cell, for example, may consist of the semiconductors: GaAs, Ge, and GaInP2. Each type of semiconductor will have a characteristic band gap energy which, loosely speaking, causes it to absorb light most efficiently at a certain color, or more precisely, to absorb electromagnetic radiation over a portion of the spectrum. The semiconductors are carefully chosen to absorb nearly all of the solar spectrum, thus generating electricity from as much of the solar energy as possible.

New solar cell technologies

Dye-sensitized solar cells (DSSCs) are made of low-cost materials and do not need elaborate equipment to manufacture. Typically a ruthenium metalorganic dye (Ru-centered) is used as a monolayer of light-absorbing material. The dye-sensitized solar cell depends on a mesoporous layer of nanoparticulate titanium dioxide to greatly amplify the surface area (200–300 m2/g TiO2, as compared to approximately 10 m2/g of flat single crystal).

The photogenerated electrons from the light absorbing dye are passed on to the n-type TiO2, and the holes are absorbed by an electrolyte on the other side of the dye. The circuit is completed by a redox couple in the electrolyte, which can be liquid or solid. This type of cell allows a more flexible use of materials, and is typically manufactured by screen printing and/or use of Ultrasonic Nozzles, with the potential for lower processing costs than those used for bulk solar cells.

However, the dyes in these cells also suffer from degradation under heat and UV light, and the cell casing is difficult to seal due to the solvents used in assembly. In spite of the above, this is a popular emerging technology with some commercial impact forecast within this decade. The first commercial shipment of DSSC solar modules occurred in July 2009 from G24i Innovations.

Organic solar cells and polymer solar cells are built from thin films (typically 100 nm) of organic semiconductors including polymers, such as polyphenylene vinylene and small-molecule compounds like copper phthalocyanine (a blue or green organic pigment) and carbon fullerenes and fullerene derivatives such as PCBM. Energy conversion efficiencies achieved to date using conductive polymers are low compared to inorganic materials.

However, it has improved quickly in the last few years and the highest NREL (National Renewable Energy Laboratory) certified efficiency has reached 8.3 percent for the Konarka Power Plastic. In addition, these cells could be beneficial for some applications where mechanical flexibility and disposability are important.

These devices differ from inorganic semiconductor solar cells in that they do not rely on the large built-in electric field of a PN junction to separate the electrons and holes created when photons are absorbed. The active region of an organic device consists of two materials, one which acts as an electron donor and the other as an acceptor.

When a photon is converted into an electron hole pair, typically in the donor material, the charges tend to remain bound in the form of an exciton, and are separated when the exciton diffuses to the donor-acceptor interface. The short exciton diffusion lengths of most polymer systems tend to limit the efficiency of such devices. Nanostructured interfaces, sometimes in the form of bulk heterojunctions, can improve performance.

Goal of high efficiency

Efficiency for solar cells is defined as the ratio of electrical energy that can be extracted and the energy of incoming radiation from the sun. The Shockley–Queisser limit refers to the maximum theoretical efficiency of a solar cell using a p-n junction to collect power from the cell.

The limit places maximum solar conversion efficiency around 33.7 percent assuming a p-n junction band gap of 1.1 eV (typical for silicon). That is, of all the power contained in sunlight falling on a silicon solar cell (about 1000 W/m²), only 33.7 percent of that could ever be turned into electricity (337 W/m²).

The limiting efficiency is usually a function of the band-gap of the absorbing material, which is illustrated in Fig. 2. The points represent the best experimental single band-gap cells fabricated to date.

Source: The Information Network, USA.

Source: The Information Network, USA.Modern commercial single-crystalline solar cells produce about 22 percent conversion efficiency, the difference due largely to practical concerns like reflection off the front surface and light blockage from the thin wires on its surface. The Shockley–Queisser limit only applies to cells with a single p-n junction; cells with multiple layers can outperform this limit. In the extreme, with an infinite number of layers, the corresponding limit is 86 percent.

New innovations is solar cell design and manufacturing are aimed at increasing the efficiency of solar cells, since the higher the efficiency of a cell, the few cells are required to achieve a set output of electricity. This is critical, particularly on space-constrained locations such as residential roofs.

SolarPA, for example, has developed a nanomaterial that can coat the surface of a completed solar cell and increase its efficiency by more than 11 percent. Thus, a cell with a 15 percent efficiency is increased to greater than 16.5 percent.

Solar shipments by type

As a supplier or potential supplier of equipment and materials to solar cell manufacturers, it is critical to determine the size and growth of the market for each type of solar cells.

In 2010, 17 Gigawatts of solar cells were shipped to customers worldwide, an increase of 139 percent over 2009 shipments. Overall, polycrystalline Si made up 79.9 percent of 2010 cell production, as shown in Fig. 3, an increase of 77.6 percent in 2009. Notably, 2010 marked the first time since 2005 that thin film market share declined (from 16.2 percent in 2009 to 14.2 percent in 2010).

Source: The Information Network, USA.

Source: The Information Network, USA.When looking at individual thin film technologies, CdTe (almost all First Solar) made up 45 percent of total thin film production in 2010, with thin film silicon and CIGS comprising 35.9 percent and 16.9 percent, respectively. CIGS was the fastest growing technology segment of PV cells, generating annual growth of 160.7 percent (albeit off a small base of 153 MW) as a number of firms moved into mid-level (60 to 80 MW) production in 2010 after years of endless hype about its promise and disruptive potential.

Still, at only 2.4 percent of the overall market, it has a long way to go before these claims can eventually be justified. Meanwhile, despite constant proclamations of its imminent demise, thin film silicon production continued to grow strongly, from only 201 MW in 2007 to 867 MW installed in 2010, and maintaining a steady overall share of 5-6 percent across this time.

Whether this technology will ever establish a leading position in the market is questionable (especially given its existing efficiency ceiling), it is far too early to write off the prospects of the more than 50 active producers in the market (most based in China and Taiwan) any time soon.

As shown in Fig. 4, by 2015 polycrystalline silicon solar cells will remain the dominant type as a stable polysilicon price environment remains in effect. The greatest growth will come from the CIGS sector, reaching 8.7 percent of the market, up from only 2.4 percent in 2010.

Source: The Information Network, USA.

Source: The Information Network, USA.Leading solar cell manufacturers

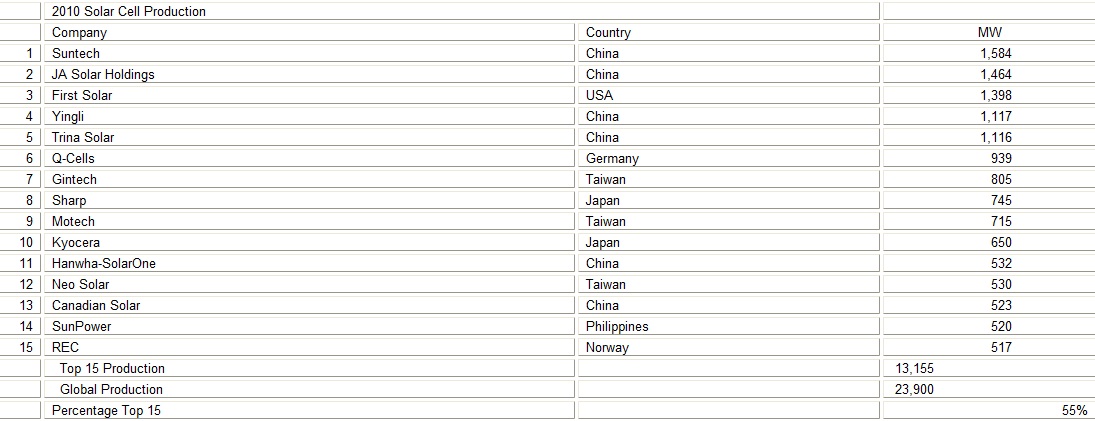

As a supplier or potential knowing who the customers are is paramount to a successful endeavor. The list of top PV cell producers is dominated by names from China and Taiwan: nine of the top fifteen cell producers are based in this region. First Solar and Sharp’s tandem-junction facility are the only thin film representatives on the list.

Source: The Information Network, USA.

Source: The Information Network, USA.Table 1 presents a list of the top 16 manufacturers of solar cells in 2010. Combined, these top 15 producers manufactured 13,155 GW of solar cells in 2010. This represented 55 percent of the total wattage of solar cells manufactured of 23,900 MW. Note that while 23,900 MW of solar cells were produced, only 17,007 MW were installed.

Table 2 lists the top 10 thin film solar cell manufacturers.

Source: The Information Network, USA.

Source: The Information Network, USA.Aside from First Solar, the size of thin film solar cell manufacturers is small. Six of the names on the list are thin film silicon producers, mostly tandem-junction based, while three CIGS firms (Solibro, Solar Frontier, and Solyndra) figure in this list. China/Taiwan presence is much more muted compared to c-Si, with only three firms (Trony, NexPower, Auria) based there.

Solar cell production by geographic region

Total cell production from the China/Taiwan region increased 152 percent, from 5,630 MW in 2009 to 14,193 MW in 2010, representing 59.4 percent of global production, up from 50 percent in 2009.

While 65 percent of solar cells were installed in Europe in 2010, only 13 percent of solar cells were manufactured there. Production increased 49 percent in Europe in 2010, while global production increased 110 percent.

Production in North America increased 93 percent in 2010. North America has a disproportionately larger share of thin film production compared to the global average, with 45 percent of total production being thin film-based. The bulk of North American c-Si cell production in 2010 came from just two firms (Solarworld USA and Suniva).

Source: The Information Network, USA.

Source: The Information Network, USA.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.